A version of this article was originally published on July 22, 2016 on Greentech Media.

By Michael O’Boyle

Like any corporation, investor-owned electric utilities have a duty to maximize shareholder profits. There’s no problem with this in principle – as long as what maximizes profits also maximizes benefits in the public interest, given utilities’ regulatory monopoly status. But today, how utilities make money must change to adapt to new grid needs, customer demands, and technological realities.

In a previous Greentech Media piece, we explained how utilities operating under cost of service regulation (COSR) achieve a regulated rate of return (r) on capital investments that ubiquitously exceeds their cost of raising funds (k), creating value for shareholders and making infrastructure investment a long-term growth strategy for most utilities, as long as r > k.

This framework works when rapid system build-out is the top goal for policymakers – i.e. when America needed to electrify every community. In fact, without a rate of return above the cost of equity for utilities, the system would stagnate because no investments would be profitable.

But when capital-based solutions are not preferred or new technology creates room for competition – i.e. today’s changing energy landscape – COSR can create disconnects between utility shareholder value and outcomes benefiting society.

To help regulators determine which utility compensation models best match shareholder revenue and societal results, we conducted research using simplified utility financial models to examine how different utility compensation approaches affect financial motivations.

New priorities require new revenue models

Today, opportunities abound for non-utility-owned, non-capital resources to meet societal goals at lower costs than conventional utility-owned capital investments. The rapid cost declines of wind and solar challenge conventional fossil fueled generation, and demand can now be dispatched alongside supply, enabling a much more flexible grid. Rapid progress on both the cost and operational effectiveness of distributed energy resources (DERs) means customers and third parties can often provide services that obviate the need for significant utility capital deployment.

Societal preferences have shifted too. For instance, many utility regulators require utilities to adopt low-carbon energy resources, while others prioritize resilience, resource diversity, or customer choice as critical outcomes.

Regulators increasingly balance these priorities with more traditional goals like customer satisfaction, safety, universal access, and affordability. Where non-capital (e.g., operational or contractual) strategies are the best fit to achieve least-cost provision of electricity and meet these societal goals, COSR is poorly suited to motivate the role society now needs utilities to play.

Regulatory alternatives

In recent years, regulators have actively examined alternative revenue models to motivate utilities to provide more efficient, reliable, and cleaner electricity service:

- In 2013, Illinois adopted a formula-based rate with a portion of returns on capital investments tied to achieving reliability metrics.

- In 2014, Xcel Energy asked Minnesota regulators to examine new revenue models based on performance.

- In 2015, Hawaii regulators started using a revenue cap for baseline capital expenditures that was indexed to GDP growth, require HECO to measure and report dozens of performance metrics, and have an open proceeding to tie performance to revenue.

- This year, the New York Public Service Commission ordered utilities receive compensation partially based on efficiency and peak demand reduction performance to reduce pollution and improve system efficiency.

- Also this year, California Public Utility Commissioner Michael Florio is examining options to pilot new utility incentives for pursuing DER alternatives.

APP’s latest research examines three cases where COSR clearly motivates utilities to pursue more expensive or dirtier investments for the greatest profit, instead of maximizing societal value. The analysis gives special focus to two fast-growing regulatory alternatives.

Comparing the revenue models

The central criterion for success in changing how utilities make money is whether the investments most valuable to society create more shareholder value (utility profit) than those failing to maximize public interest – defined as not only overall cost savings, but also environmental performance. While utilities must invest in poles, wires, capacitors, and grid modernization, DERs and operational changes can often save customers money while improving customer satisfaction and cleaning up generation. APP’s latest research tests scenarios where DERs provide equivalent service at a lower price, finding that new revenue models can help unlock untapped opportunities.

For example, we considered three solutions to meet demand growth on a distribution circuit. Assuming a substation upgrade would be considerably more expensive than procuring local DERs (based in part on estimates from the Brooklyn Queens Demand Management Project), we found that PIMs and a well-designed revenue cap better aligned customer value with utility motivation.

In a second example, we looked at operational solutions as an alternative to grid modernization investment, in particular whether utilities would be motivated to invest in fiber optic cables for a communications network or take advantage of existing networks at a lower cost under various revenue models. Unsurprisingly, utilities were rewarded for laying cables under COSR, but would likely pursue a cost-effective non-utility-owned option under a revenue cap.

In our last model, we examined the impact of a greenhouse gas emissions performance incentive on a utility’s decision to either build a new natural gas plant or a combination of centralized and distributed clean resources. The choice became quite clear for the utility under the PIM: A clean, distributed alternative would maximize the public good and utility profit at the same time.

Takeaways

Examined together, the financial models produced three key takeaways:

- COSR creates utility incentives misaligned with societal value in scenarios where non-infrastructure or non-utility-owned alternatives are superior from a societal perspective.

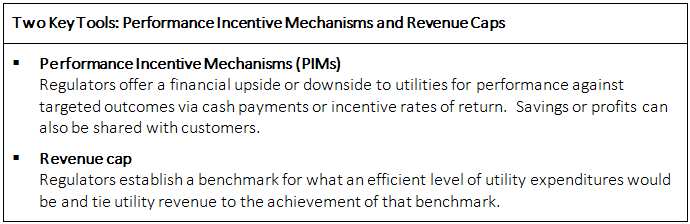

- PIMs hold the potential to monetize presently uncaptured benefits and costs in utility regulation, and to motivate utilities to perform against outcomes that society prioritizes.

- Multi-year revenue caps can be a powerful tool to align utility shareholder value with non-infrastructure-based strategies to meet grid needs. These tools deserve greater consideration, alongside PIMs, in utility regulatory model discussions.

Regulatory models should not be examined in a vacuum, however, and implementing each of the regulatory models presents real risks. For example, the powerful incentives created by revenue caps mean they must be set at the right level or else risk unintended consequences. In areas where a preferred alternative provides non-monetized societal value, PIMs can be used to motivate desirable project attributes, but may create undue compensation swings if the targets fail to anticipate technological potential or fail to adjust for macroeconomic or weather impacts outside the utility’s control.

Recommendations for policymakers

Gradual approaches reduce utility and customer risk, so regulators and utilities should consider incremental steps to move toward revenue models meeting 21st century electricity system goals:

- Jurisdictions interested in using PIMs to modify traditional regulation could start by beginning to measure important metrics, and then add targets with low financial stakes.

- A revenue cap could begin with a narrow band of allowed returns, where deviations from this band trigger automatic adjustments to the cap.

- Alternatively, regulators could apply a revenue cap to a specific subset of expenditures, such as grid modernization, where non-conventional strategies are likely to exist.

- Utilities could begin collecting more distribution system information to identify value opportunities and regulators could require integrated distribution planning alongside new revenue models.

Today’s shifting energy landscape means COSR won’t always align utility motivation with societal value. As we move toward the utility of the future, we must ask if revenue models are driving the right investments. There are alternatives to COSR that better align utility models with societal values – and it’s in regulators’ power to take steps toward them.