This post was originally published on The Energy Collective on September 23, 2015.

This month the experts of America’s Power Plan released a new resource for policymakers and electric utility stakeholders as a part of our work under the Solar Electric Power Association’s (SEPA) 51st State Challenge. The new report begins to answer the question – “Who should own and operate distributed energy resources?” The report examines a series of case studies on different ownership models for distributed energy resources (DERs) with system optimization as the metric for success. It turns out that there are many options for who can own and operate DERs—and any of them can work, as long as the revenue streams (and revenue delivery mechanisms) are designed or adjusted appropriately.

The new paper functions as an addendum to America’s Power Plan’s original 51st State submission, An Adaptive Approach to Promote System Optimization, by Michael O’Boyle. This concept paper, which was selected as a top concept to feature at SEPA’s summit in April, described fundamental principles of rate design and market structure that can help states better support technological innovation and grid efficiency. Recognizing that approaches will vary across the nation, the paper advocates for a reorientation of regulation toward the outcomes consumers want most from the electricity system: affordable, reliable, environmentally clean electricity service.

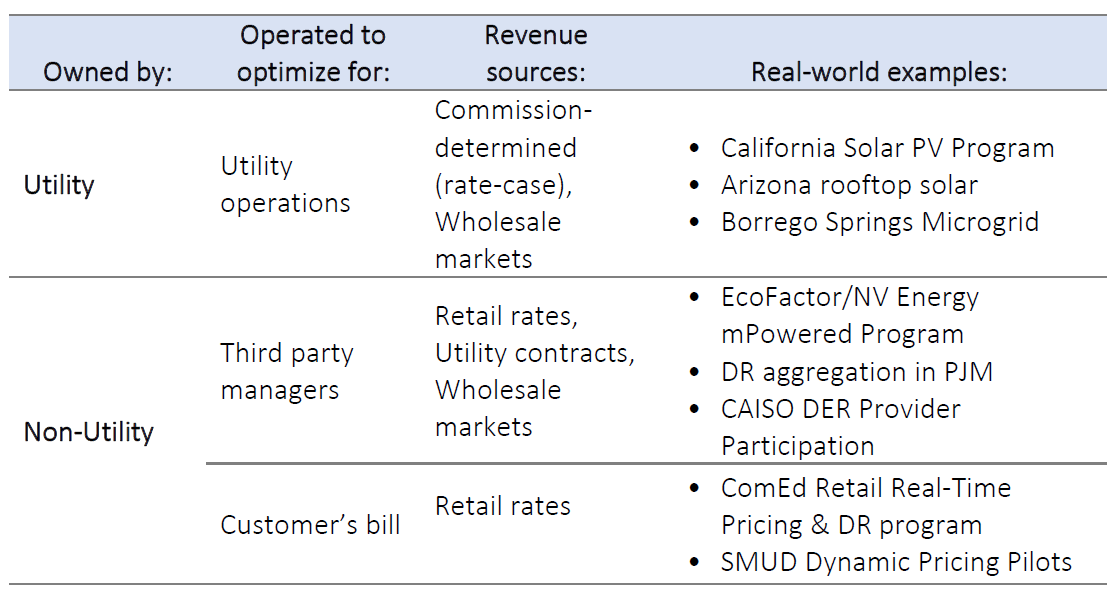

Who Should Own and Operate Distributed Energy Resources? applies these principles to three different models of distributed energy resource ownership and operation: utility-owned and operated DERs, third party-operated DERs, and customer-operated DERs. The paper identifies strengths and weaknesses in each approach, with an eye toward recommending complementary policies to consider depending on which ownership and operation structure a region chooses. This table categorizes the case studies included in this report:

Each of these case studies draws on experience with different approaches to tackling the same problem: how to take advantage of cost-effective distributed technologies that have run into outdated regulatory models. Any of these ownership and operation models can improve system optimization so long as the value proposition to each actor aligns with the public interest.

Utility owned and operated DERs

The utility-owned and operated model may be able to demonstrate and accelerate early deployment of new technologies, as in the case of the California Solar PV Program (SPVP) and Borrego Springs Microgrid. However, when utility-owned DERs play in competitive markets, they may either crowd out competitors or result in inferior performance.

One way to support emerging technologies and avoid cost overruns in a utility-owned structure is to tie program-related utility revenue to specific, quantitative performance outcomes. This minimizes the investment risk for customers. Another way is to allow utilities to pilot DERs—in parallel with third-party alternatives—again with clear metrics for performance. Regulators can reevaluate the programs periodically, as was the case with California’s Solar PV Program and Arizona’s rooftop solar programs.

One emerging example of this kind of parallel piloting is Central Hudson’s May 1 proposal to own and operate community solar alongside SolarCity as part of a demonstration project under New York’s Reforming the Energy Vision initiative. This pilot program will allow comparison of a third-party community solar model with a utility-owned model. SDG&E also recently proposed two sister pilot programs under its distributed resource plan that will compare utility owned and operated storage with a customer-centric storage model that includes a dynamic rate. Each will help to define the evolving boundaries of the “natural monopoly” and competition on the distribution system.

Third-Party and Customer-operated DERs

The third-party and customer-owned and operated DERs have been effective at maximizing the revenue available to them, but can improve performance as well if the available revenue streams are better aligned with the public interest, and if third-parties can access system data from utilities. For example, dynamic rates that better track the value of demand response could increase the savings and responsiveness of customers participating in NV Energy’s EcoFactor program, which is a demand response and home energy management program that uses an internet-connected smart thermostat and interacts with the customer’s air conditioner.

Customer-centric programs could also improve if customers can get paid for the full value DERs provide to the bulk and distribution systems, including external value (such as environmental benefit). ComEd’s Residential Real-Time Pricing (RRTP) program, for example, could evolve to include a varying distribution charge that compensates customers for on-site generation on top of avoided energy costs. Value of Solar Tariffs in Minnesota and Austin Energy are examples of how this can work in practice for a specific resource (distributed solar), but the dynamic interaction between the bulk system and distribution optimization still requires refinement.

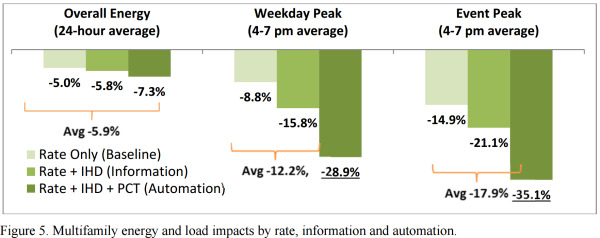

Technology can enable consumers to better optimize their behavior against more complex rate designs. When automation technologies (like programmable communicating thermostats) are paired with rates designed to promote optimal deployment of customer DERs, as in the Sacramento Municipal Utility District (SMUD) Multifamily Summer Solutions (MSS) Study, customer demand response (and parallel savings) improve dramatically:

Source: ACEEE 2014

+++

The original principles articulated in An Adaptive Approach to Promote System Optimization can help guide experimentation with all of these models of DER ownership and operation. Fair valuation of DERs is key to ensuring they can compete with centralized generation to meet system needs at least cost. Likewise, integration of new technologies through any model should be iterative to minimize the risk to utility customers. To the extent possible, new rate design should be coupled with enabling technologies and third-party data access to ensure that complementary technologies can help customers optimize their bills and maximize system benefits. No one model will fit every state or utility; but with the right framework and complementary policies, each model can support an optimized grid system.