A version of this article was originally published on August 24, 2015 on Greentech Media.

By Sonia Aggarwal, Steve Kihm, and Ron Lehr

Utility managers pay attention to Wall Street, and often more can be learned about utilities’ top priorities by listening to shareholder earnings calls than regulatory proceedings. As with any investor-owned company, managers of investor-owned utilities are obligated to maximize shareholder value. So it pays when regulators can find ways to align shareholder value creation with the public interest. Enter performance-based regulation. Efforts in this regard are underway across the nation—in states like Minnesota, Illinois, and New York.

Regulatory finance, distilled

When a utility manager considers whether or not to make an investment, he or she is looking at whether the allowed return on that investment (r) is less or greater than the cost of the capital required (k). The return (r) is an accounting-based return for the firm; the cost (k) is a market-based return for its investors. The difference between r and k is the engine that drives stock price. Regulators can set r¸ but the financial markets on Wall Street determine k.

Over time, these two terms have been conflated; many believe the rate of return is the same as the cost of capital. But these two terms are conceptually different, and are most often different in numerical value as well. You Get What You Pay For: Moving toward Value in Utility Compensation exposes these terms—and their import for utility regulation and management—in more detail.

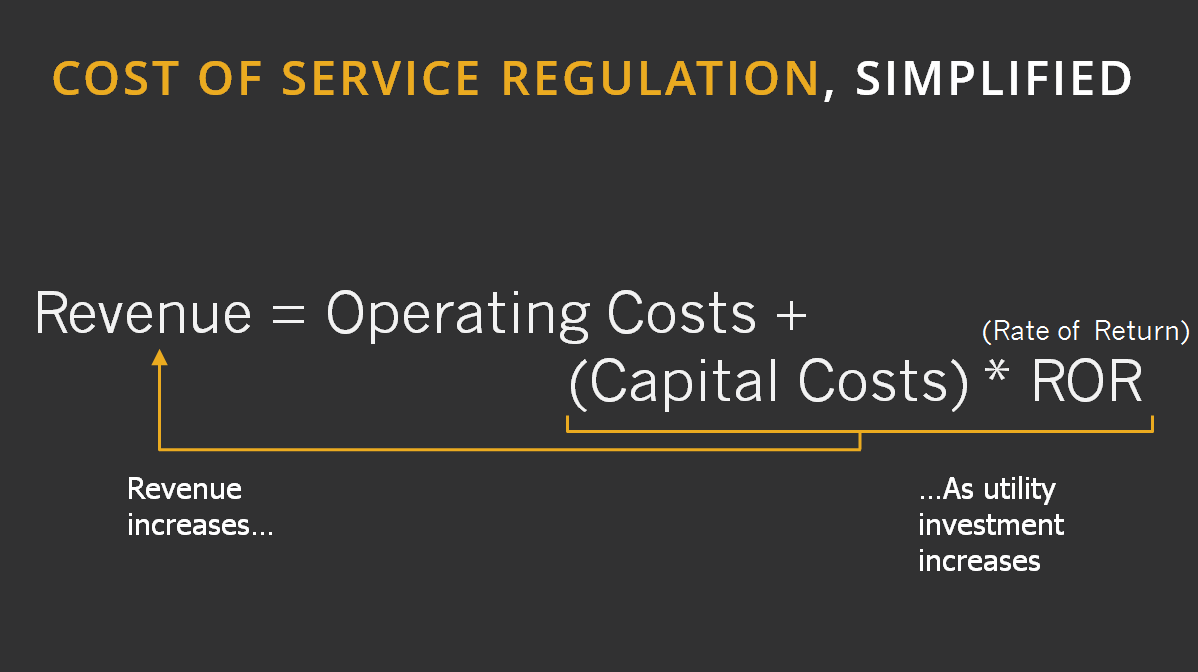

Under the traditional cost-of-service regulatory model, all prudent capital investments earn the same rate of return, which empirical evidence shows is generally higher than the cost of capital. With returns exceeding the costs of capital, IOUs create investor value with every prudent capital investment and utility management is therefore motivated to spend capital. (On the other hand, if the return were equal to the cost of capital utilities would have no incentive to invest in any project.) Creating an incentive to invest was appropriate when the primary social goal of the utility sector was to grow enough to provide universal service, and economies of scale were clear. But given flat-lining demand, system build-out is no longer the primary objective. Having accomplished the first wave of goals for the power sector, several states are considering how to realign utility incentives with today’s customer- and societal-goals.

Using performance-based regulation to create value

Regulators can use the value engine (r-k) to align utilities’ financial motivations with delivering value to customers and society. If utilities have the opportunity to create shareholder value by investing in assets that improve performance, but can only recover basic costs if they invest in others, utilities will seek the value-creating investments. This is not a new idea; in his classic 1970 text The Economics of Regulation, Alfred Kahn argues that the value of utilities should closely track their performance:

“The rate of return . . . must provide the incentives to private management that competition and profit-maximization are supposed to provide in the nonregulated private economy generally . . . permitting all regulated companies as a matter of course to earn rates of return in excess of the cost of capital does not supply the answer; there has to be some means of . . . identifying the companies that have been unusually enterprising or efficient and offering higher profits to them while denying them to others.”

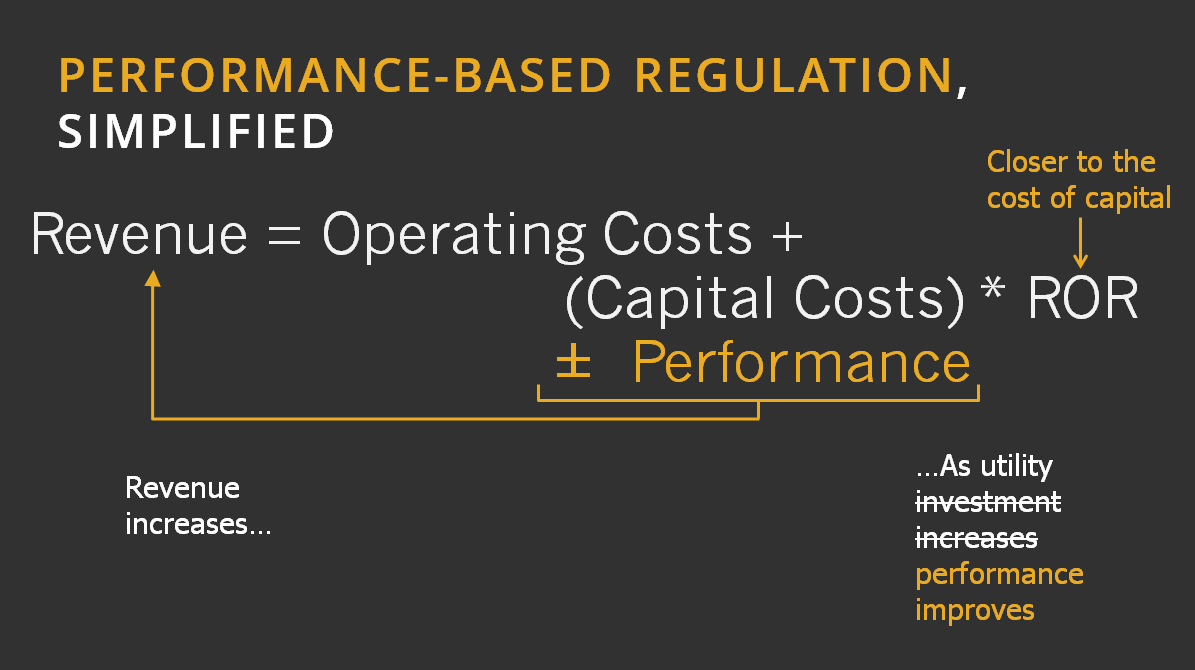

Under performance-based regulation, utilities do not necessarily earn returns in excess of the cost of equity on all investments. Regulators can amplify (r-k) when utilities deliver value to customers and achieve public policy objectives, and shrink it when they fail to do so.

The latest developments in New York

In April of 2014, New York announced six goals for its “Reforming the Energy Vision” proceeding:

- Enhanced customer knowledge and tools that will support effective management of the total energy bill;

- Market animation and leverage of customer contributions;

- System wide efficiency;

- Fuel and resource diversity;

- System reliability and resiliency; and

- Reduction of carbon emissions.

The proceeding was separated into two tracks, with Track One focused on developing distributed resource markets, and Track Two focused on reforming utility ratemaking practices. These six public policy goals would form the basis for new ratemaking practices under Track Two, which sought to “align utilities’ financial interests with the objectives of reform.” Public Service Commission staff released the Track Two proposal at the end of last month.

Track 2 uses three tools to align utility shareholder value with the original goals: earnings incentive mechanisms, measuring (but not monetizing) other performance metrics, and reforming the clawback mechanism.

- Earnings incentive mechanisms supplement the rate of return with basis point adjustments tied to performance, using the shareholder “value engine” to increase (r-k) as performance improves. New York PSC staff recommends that peak reduction, energy efficiency, customer engagement and information access, affordability, and interconnection be measured and monetized as earnings incentive mechanisms.

- Additional performance metrics will be measured but not monetized. Tracking these metrics encourages some management focus, offers an incremental step toward possible monetization in the future, and provides transparency for stakeholders. Carbon emissions, despite being one of the six main objectives of REV, is notably measured but unmonetized.

- The staff also proposes reforming the “clawback” mechanism by which capital expenditures are adjusted in each rate case. Rather than punish utilities for revising capital expenses downward, the new clawback would allow utilities to keep the difference between planned capital expenditures and cheaper third-party DER solutions.

These reforms are the first steps toward aligning utility shareholder value with customer- and societal-goals in New York.

Financial impacts of performance-based regulation

As states move toward performance-based regulation, it will be important to ensure that utilities remain in a favorable position to attract capital. Shareholders and their agents—utility managers—need to see that the financial value engine can support adequate returns on investments as utilities deliver more value to customers and society.

A new system of utility compensation need not be perfect from the start; it only needs to improve upon the current one. The good news: current approaches set a relatively low bar. Today’s system determines utility compensation via rate cases that typically happen after the utility has already made its investment decisions, meaning that the investment is completely at risk until a rate case order is issued. Under new approaches to compensation, these investment risks can be better managed, and possibly more transparently from an investment analytical perspective—and those risk calculations can guide utility investment toward assets that customers and society value.

Concrete steps for policymakers to use the value engine to improve performance

Based on the ideas laid out here and this paper, these five steps can transform regulation into a forward-looking system that creates customer- and societal-value:

- Engage stakeholders to consider which customer- and societal-values are most important for the regulated electric sector in your region. Drive toward quantitative metrics for performance in each category. This handbook from Synapse provides examples of quantifiable metrics for utility performance.

- Improve estimates of the utility’s cost of equity so that they reflect the minimum markup on money they receive from shareholders. This should set the lower bound for the return on equity allowed to utilities.

- Research the benefits in each of the value categories—estimating total benefits can set an upper bound for the incentives offered to utilities that deliver these values.

- Consider the difference between the cost of equity and the current return on equity – this is the money that motivates shareholders and utility management, and represents the existing or baseline incentive for performance against which future incentives should be measured.

- Consider alternative ways to deliver the performance portion of utility revenues, aside from adjustments to rate of return, keeping in mind that direct shareholder incentives (or, better yet, “shared savings” programs where some of the incentive goes to the shareholder and some flows back to the customer) may provide the most direct connection to performance in the value category intended for the policy to achieve.

Utility executives and financial analysts need to see that the financial value engine can work to support adequate returns on investments as the electricity system, the regulatory model, and utility incentives evolve. If regulators follow these five steps, they can give utilities that assurance, and put the power system on track to deliver more value to customers and society.